Inflation is the topic du jour in global financial markets.

The parameters of the debate appear to be focussed on the likelihood of some persistent inflation, and potential financial stability concerns, in the absence of a timely withdrawal of the historically high levels of monetary accommodation currently being applied by central banks.

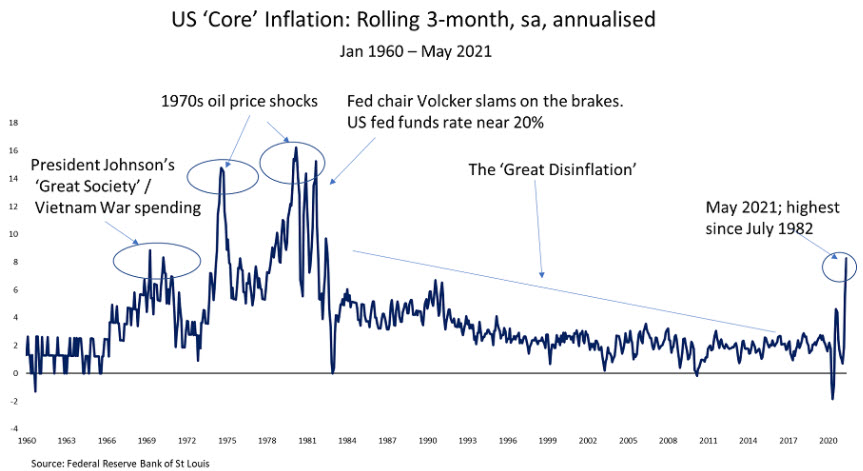

In the US the most recent May inflation report showed annual ‘core’ inflation at its highest level since 1992. In the past three months US inflation was running at an annual rate of 8.3%, the highest since 1982.

, a sponsor of Firstlinks. He has previously worked in The Treasury and in the office of the then Treasurer, Paul Keating, from 1983-88. The views expressed are his own and do not consider the circumstances of any investor.

, a sponsor of Firstlinks. He has previously worked in The Treasury and in the office of the then Treasurer, Paul Keating, from 1983-88. The views expressed are his own and do not consider the circumstances of any investor.