Gold prices have been in a corrective pattern for the past 12 months, having fallen by approximately 12% in US dollar terms since hitting all-time highs in August last year.

This pullback was not unexpected given how fast gold had run up in recent times, with the precious metal rallying by almost 75% in the two years leading into its August 2020 peak. Bullish momentum had clearly run its course, while other factors contributing to the correction include:

- A strong rally in equities, with the S&P 500 now having doubled from its Q1 2020 lows.

- Confidence in vaccine rollout across most of the developed world.

- Stabilisation in real yields.

- The market’s belief that the current spike in inflation will prove transitory.

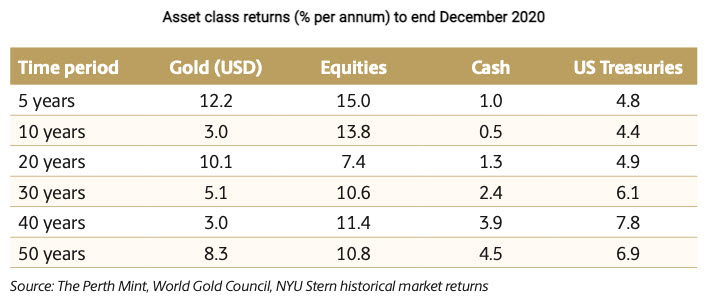

History may come to judge the last year’s gold price pullback as the culmination of a tough decade for precious metal bulls, seen in the table below highlighting the performance of gold and more traditional asset classes over the short, medium and long-term.

from August 2011 that found 34% of Americans thought gold was the best long-term investment.

from August 2011 that found 34% of Americans thought gold was the best long-term investment.

While gold has historically delivered a range of portfolio benefits that a broader basket of commodities can’t replicate, a profound bear market in commodities still represents a headwind for the precious metal.

The decade ahead

While gold has been in a corrective pattern for the last year, a solid case can be made that the coming decade will be more favourable to the precious metal.

Factors supporting this conclusion include:

- Sentiment toward gold has shiftedIn a complete reversal of the situation gold found itself in as it was heading towards USD 1,900 per troy ounce in 2011, the precious metal is now largely unloved by investors, who are far more convinced that stocks and real estate are the safer long-term bet. This can be seen in the table below, which is drawn from Gallup poll data from 2011 to 2021.On a relative basis, gold is as unloved as it has ever been compared to real estate, while it is still far less popular than equities are today.Data like this doesn’t prove anything per se, but these are the kind of signals one would expect to see when a market is close to bottoming. By way of reference, gold today is essentially as popular as equities were back in 2011. The S&P 500 has rallied by more than 230% since then.

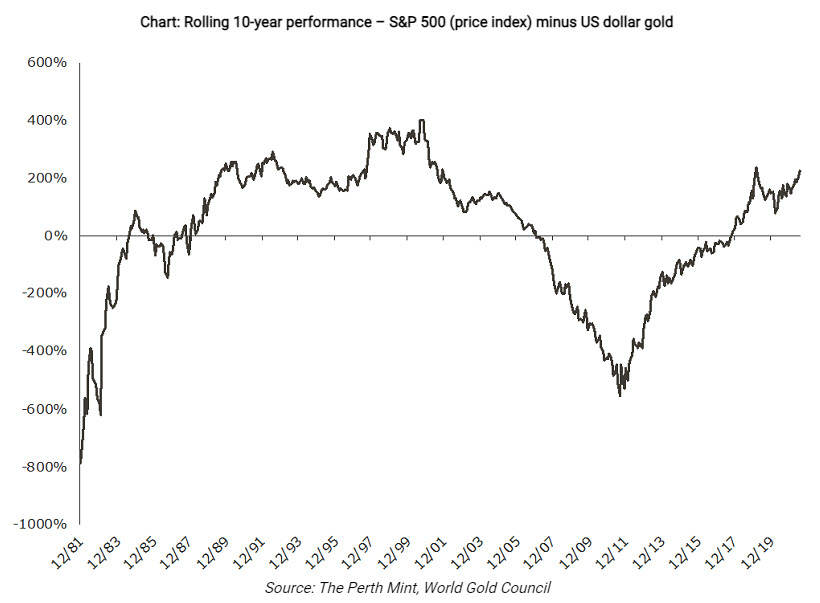

- Extreme equity market outperformanceThe relative performance of equities versus gold is the complete opposite today as compared to late 2011, when gold hit its last peak. Back then, gold had outperformed the S&P 500 by more than 500% on a 10-year basis.By the end of July 2021, gold was underperforming the S&P 500 by more than 225%, with the rolling 10-year performance differential between the two seen in the chart below.