Among my various investment activities, I am the Portfolio Manager of the $110 million Australian Philanthropic Services Foundation (APS Foundation). This article focuses on how I have navigated the uncertainties and wild gyrations of investment markets during the COVID-19 pandemic and benefited from a relatively-large holding in private debt securities.

What is a public ancillary fund?

The APS Foundation is a communal philanthropic structure called a public ancillary fund, a structure which is very efficient and tax effective for people interested in philanthropy. It is particularly attractive to those who need a tax deduction now but want the flexibility to undertake a regular flow of charitable giving over time.

At this time of year, APS Foundation attracts a lot of attention as people think about philanthropy and do their tax planning and prepare for the close of another financial year. I feel the privilege, excitement and ‘pressure’ of managing this Foundation and take it very seriously. The onset of the COVID-19 pandemic and resultant negative economic and market consequences have given me plenty to think about. Sometimes the words ‘cold sweat’ come to mind when investment markets fall 20%-30% virtually overnight and I think about how that may impact the APS Foundation and in turn its impact on the community!

The APS Foundation comprises around 300 giving funds (also known as sub-funds) established by individuals, families and companies. They make a tax-deductible donation of at least $50,000 to the Foundation, which is set aside into their own-named giving fund. Each year at least 4% of the giving-fund balance is given to charities recommended by the fund holder. The giving funds are pooled and invested together, with investment returns accruing to the underlying giving funds. Returns are tax-free, so good investment management can see the balance grow, increasing the amount for charities over time.

Investment objectives and strategy

The investment objective for the APS Foundation is to achieve a return after fees at least equal to CPI inflation +4% per annum, measured over rolling seven-year periods. A lot of factors were taken into account before landing on this objective, including:

- the need to distribute a minimum of 4% per annum to charities,

- the likelihood of inflation affecting the value of the investments and income generated,

- the risk of capital or income loss,

- the liquidity of the investments,

- the costs of investment alternatives and transactions, and

- the benefits of diversification of investments.

With these investment objectives in mind, we set broad investment ranges to ensure we have plenty of flexibility.

I decided long ago that it was paramount that a charitable foundation, like APS Foundation, needed to have a well-diversified investment portfolio. That would be my best protection against unexpected negative surprises that investment markets have a habit of delivering more often than we sometimes think.

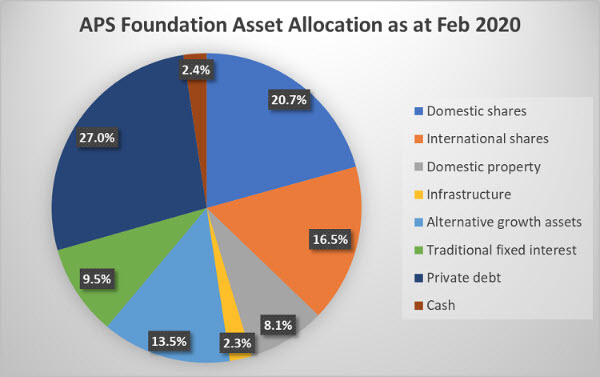

As at the end of February 2020 (just before COVID-19 started to hit hard) the asset allocation of the APS Foundation was as follows: