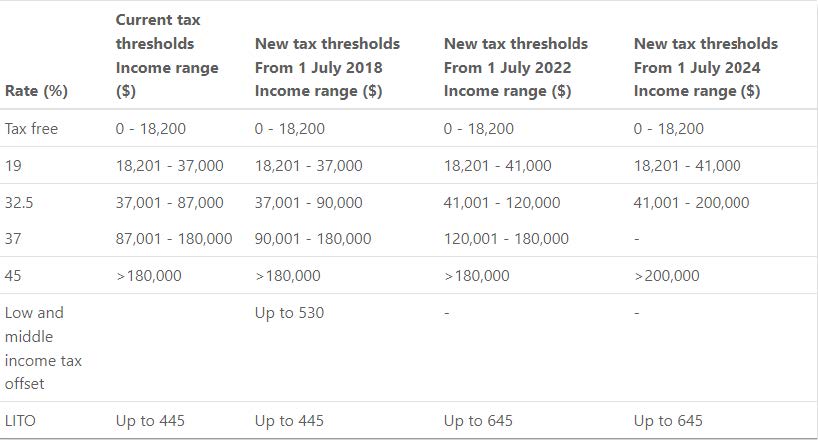

Personal Income Tax

The Government is introducing a seven year Personal Income Tax Plan.

The first step provides permanent tax relief to low and middle-income earners to help with the cost of living pressures.

The second step provides relief from bracket creep by increasing the top threshold of the 32.5 percent personal income tax bracket.

The third step simplifies and flattens the system by removing the 37 percent income tax bracket entirely.

Step 1 – Targeted tax relief for low and middle-income earners

- A Low and Middle Income Tax Offset (LAMITO) will be introduced – a non-refundable tax offset of up to $530 per annum to Australian resident low and middle income taxpayers. It will be available for the 2018/19 to 2021/22 tax years and will be received as a lump sum on assessment after an individual lodges their tax return.

- The LAMITO will provide a benefit of up to $200 for taxpayers with taxable income of $37,000 or less. Between $37,000 and $48,000 the value of the offset will increase at a rate of three cents per dollar to the maximum of $530. Taxpayers with taxable incomes from $48,001 to $90,000 will be eligible for the maximum benefit of $530. From $90,001 to $125,333, the offset will phase out at a rate of 1.5 cents per dollar.

- The LAMITO is in addition to the existing Low Income Tax Offset (LITO).

Step 2 – Protecting middle income earners from bracket creep

- From 1 July 2018, the top threshold of the 32.5 percent personal income tax bracket will increase from $87,000 to $90,000.

- From 1 July 2022, the LITO will increase from $445 to $645 and the top threshold of the 19 percent income tax bracket will increase from $37,000 to $41,000 to lock in the benefits of Step 1.

- The increased LITO will be withdrawn at a rate of 6.5 cents per dollar between incomes of $37,000 and $41,000, and at a rate of 1.5 cents per dollar between incomes of $41,001 and $66,667.

- From 1 July 2022, the top threshold of the 32.5 percent income tax bracket will increase from $90,000 to $120,000.

Step 3 – Ensuring Australians pay less tax by making the system simpler

- From 1 July 2024, the top threshold of the 32.5 percent income tax bracket will increase from $120,000 to $200,000. Thus, taxpayers will pay the top marginal tax rate of 45 percent from taxable incomes exceeding $200,000 and the 32.5 percent tax bracket will apply to taxable incomes of $41,001 to $200,000.

New personal tax rates & thresholds

This increase in fund membership will help small business owners and families comprising say mum and dad and up to four children (or two children with their spouses) set-up an SMSF, especially where a family business, including a family farm, operating over several generations is involved. However, this won’t come without its own problems and complexity! Whilst the Cooper Review several years ago recommended increasing the number of members to 10, the Government’s initiative now to increase membership could be seen as a means of combating the ALP’s proposal to stop franking credit refunds. Currently, less than 5 percent of SMSFs have three or four members.

Also, Superstream will be extended to include SMSFs which means that members can initiate rollovers between mainstream public offer (retail) and industry funds and their SMSF electronically – making it easier and faster!

Changes still in the pipeline

With little change to super in this year’s Federal Budget, there’s time to both catch-up on things arising from recent changes that must be done and prepare for those changes still in the pipeline.

We now have time for the ‘dust to settle’ … to a certain extent!

Here’s a re-cap of the more significant superannuation changes to deal with now and those that are in the pipeline.

Federal Budget 2016 – the start of the super reforms

Two years ago in the 2016 Federal Budget, the Treasurer announced the most significant changes to super in a decade with the introduction of the superannuation reforms.

We’re only just embarking on a regime that’s going to take time to digest. One fraught with danger and a real minefield for the unwary. Now more than ever, the need for quality financial advice is critical!

Just take the ability to make a simple personal after-tax contribution for example.

We’ve just had a decade where the non-concessional (after-tax) contributions cap was relatively straightforward, ending with simply $180,000 a year or, for people under age 65 at 1 July in a financial year, $540,000 over a three-year period – and people still got it wrong!

Now, whether or not you can make an after-tax contribution depends on how much you’ve got in super. If your TSB at 30 June 2017 is less than $1.6 million then you can contribute, provided you’re eligible, i.e. you’re not too old and if you are, whether you meet the work test. The bring-forward rule – your ability to increase your current year’s contribution by utilising the cap otherwise applicable in the next few years and the amount – depends on your age and how close your super is to $1.6 million. Also, what you’ve contributed in the past two years may come into play. Understandably, there’s going to be mistakes if you’re not extremely careful or you don’t seek expert advice!

Employees who ceased making salary sacrifice contributions to instead make their own personal deductible contribution(s) for the first time will need to get their ‘financial house in order’ to do so before 30 June. Not only must you make the contribution but you must also provide the super fund trustee with a notice of intent (NOI) to claim a tax deduction for the contribution. Be careful not to touch the contribution, i.e. roll it over to another fund, withdraw it, or start an income stream, before first lodging your NOI. A new experience for employees!

Accountants and financial advisers are still grappling with transitional capital gains tax (CGT) relief in the lead up to 30 June when many SMSF annual returns are due for lodgement. This is another important but complex measure arising from the super reforms.

CGT relief is the opportunity, where certain conditions are met, to reset the cost base of a fund’s asset(s) to market value where a member was required to reduce their retirement phase pension balance to $1.6 million by 1 July 2017 or they had a transition to retirement pension (of any value).

Last of the super reforms starting soon!

There is one final measure announced in the 2016 Federal Budget still to come into play from 1 July this year. It is the last and one of the few favourable measures to come out of the superannuation reforms. It is the ability to carry forward any unused concessional (pre-tax) contributions cap amount arising from 1 July 2018. Any unused amount can be carried forward on a rolling five-year basis and can only be used if your TSB is less than $500,000.

For example, if you and/or your employer only make concessional contributions of say $20,000 in 2018/19 – a shortfall of $5,000 from the concessional contributions cap of $25,000 – you can carry forward $5,000. Then, in 2019/20 you and/or your employer could, if you choose, make concessional contributions up to $30,000, provided your TSB is under $500,000.

This measure was implemented primarily to help people, especially women, temporarily off work, for example to raise children, to top-up their super savings once they re-enter the workforce. However, carrying forward unused concessional contributions cap amounts into future years may now reduce the tax effectiveness of those contributions given the reduced personal income tax rates.

Federal Budget 2017 – mixing super and housing!

In the 2017 Federal Budget the Treasurer introduced certain measures to address housing affordability. Two such measures were thrown into the superannuation arena which will soon take traction.

- The First Home Super Saver Scheme. This scheme allows people to save for your first home in the concessionally taxed super system. Since 1 July 2017, people saving for their first home could make voluntary contributions (both concessional and non-concessional) into their super fund. Then, starting from 1 July this year, people can apply, provided they’re eligible, for the release of their voluntary contributions together with associated earnings to help purchase their first home.

- ‘Downsizer contributions’. From 1 July this year if you sell your home owned by you or your spouse for a continuous period of at least 10 years and you are aged 65 or more then you may be able to contribute some or all the sale proceeds into super. These contributions, known as ‘downsizer contributions’, allow you to boost your super savings even if you’re otherwise ineligible to contribute under superannuation law due to your age, work status or the amount you’ve got in super, i.e. TSB.

To download the above article, please click here.