The Retirement Income Review (RIR) noted that many retirees leave large bequests and they would have enjoyed a higher standard of living in retirement if only they had spent some of their capital, not just the income from their investments. Planning cash flow in retirement is extremely difficult because of the uncertainties about expenditure, doubts about investment returns and unpredictability about how long we are going to live.

How long before the tank is empty?

For some retirees, investment returns exceed withdrawals, their savings nest egg continues to accumulate, and they need never fear outliving their savings.

For many others, retirement savings can be compared with a rain water tank. Cash flows in from investment income and the sale of assets and cash flows out to pay a regular income stream as well as lump sums. Just like a rain water tank, if the cash outflow is greater than the cash inflow, sooner or later the tank is empty. The critical question then is; “How long before the retirement savings are exhausted?” The advice is typically; “It depends…” It depends on so many uncertainties that many retirees become extremely cautious.

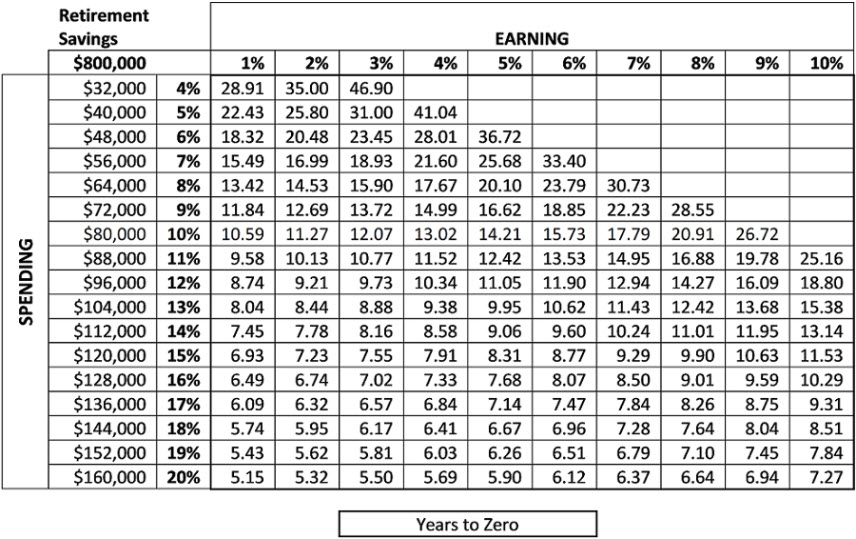

Rather than simply hoping for the best, the table below provides some guidance for that planning. It shows the number of years it takes for a starting amount of savings to reduce to zero if the percentage withdrawn is greater than the percentage income earned.

To make the spending percentages meaningful, I have included a nominal capital value of retirement savings. Please note the starting capital amount is irrelevant in determining how long it will last. What matters, as always, is the earning rate and the withdrawal rate.

Spending more than you earn

Assume Sue has $800,000 in savings and she needs an annual income of $64,000 (8%). Assume also these retirement savings are invested and earning 6%. Therefore, Sue needs to liquidate $16,000 of capital in the first year to pay the shortfall in income and her savings balance progressively declines. According to this table, reading across the rows and down the columns, it will take 23.79 years until those retirement savings are reduced to zero.

If Sue could reduce her spending to 7%, her savings will last for 33.4 years.

The table shows that if Sue spends 8% of her savings annually and earns only 1% per year, from a term deposit for example, her savings will be exhausted in only 13.42 years. It begs the question why term deposits remain so popular with retirees.

This table assumes constant withdrawal and earning rates over the whole time period, and it assumes no fees, taxes or inflation. The table is not a prediction but it can be instructive.