Anyone who has an account-based pension knows they must take a minimum payment each year. Of course, those requiring more income can take it, however, there are people who do not need this payment because they have other sources of income to live on, but still want to be in retirement phase for the tax benefits. For them it’s inconvenient to be forced to take a minimum payment, particularly when they need to sell assets to make the payment.

Earlier this year, the pension drawdown requirements were temporarily reduced as part of a package of financial assistance the Coalition Government provided to Australians to address the economic downturn resulting from COVID-19.

This change—identical to the one implemented by the Labor Government during the Global Financial Crisis—is designed to help retirees manage the impact of the volatility in financial markets on their retirement savings.

It reduces the pressure on super funds to sell assets at depressed prices to fund members’ pension payments—avoiding a fire sale of growth assets in a market downturn helps preserve retirees’ capital.

So, halving the minimum drawdown in 2019/20 was a welcome relief, especially the way the economy was performing. And the good news is this reduction continues for 2020/21.

In addition to account-based pensions, the 50 per cent reduction applies to transition-to-retirement pensions, allocated pensions and market-linked pensions (i.e. term allocated pensions), but it does not apply to complying lifetime or life expectancy pensions, flexi pensions or any defined benefit pension requiring an actuarial certificate.

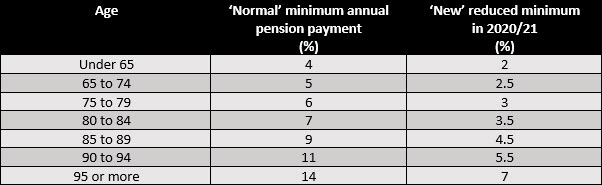

It means for people aged 65 to 74, instead of having to draw a minimum annual payment of 5 per cent, it is now 2.5 per cent. For those aged 75 to 79, it’s now 3 per cent, not 6 per cent, and so on.

Get it right

If you’re running your own SMSF and doing things yourself, ensure you get the calculation right.

Take Geraldine, aged 68, who has an account-based pension in her SMSF which had an account balance at 1 July 2020 of $640,220. The ‘normal’ minimum annual payment is $32,010 (5% x $640,220 rounded to nearest $10) and the ‘new’ minimum is $16,010 (2.5% x $640,220 rounded to nearest $10).

Seems straightforward enough and it is.

However, if Geraldine just halves the ‘normal’ minimum and pays $16,005 (50% x $32,010), then she’ll have got it wrong and her SMSF will fail to meet the minimum pension standards. The underpayment of $5 will be a real headache because her account-based pension will be taken to have ceased at 1 July 2020—unless the Commissioner of Taxation allows the income stream to continue on the basis that specific conditions are met.

Consequently, her SMSF may lose the tax benefit of being in retirement phase with earnings, including capital gains, no longer being tax-free—instead becoming taxable at up to 15 percent—and any payments during the year become lump sums for both tax and super law purposes.

When you need more than the ‘new’ reduced minimum

If you require more income than what the ‘new’ reduced minimum payment provides, you can always take more. However, depending on your circumstances, consider taking the amount above the ‘new’ minimum as a lump sum withdrawal—a ‘partial commutation’ of your income stream—rather than as pension income.

You might to do this if you have—or see yourself having—a problem with the transfer balance cap (TBC), currently $1.6 million, i.e. the maximum you can move into the tax-free retirement phase.

Making a lump sum withdrawal reduces the amount counting towards your TBC, so you can transfer more into retirement phase later.

For example, you may need room with your TBC when your spouse dies and you receive their super as a death benefit income stream, or their pension ‘reverts’—automatically continues to be paid—to you.

You may want to convert contributions you and/or an employer may still be making into an income stream one day. If you are 67 or more, retired and otherwise ineligible to contribute, this contribution may come from the proceeds of selling your home, i.e. a ‘downsizer contribution’.

Or you might have money sitting in an accumulation account you’d like to start a pension with but been unable to due to the TBC—although if this was the case, you would draw your additional income needs from that account in the first place.

Back to Geraldine

Geraldine’s ‘normal’ minimum is $32,010 and her ‘new’ reduced minimum is $16,010, but she needs the ‘normal’ minimum amount—in addition to another super income stream she is receiving—to fund her lifestyle needs.

Accordingly, she can take $32,010 in pension payments, or $16,010 as pension income and $16,000 as a lump sum withdrawal(s)—partial commutation(s). Either way she gets $32,010 from her account-based pension.

What’s the difference?

The difference involves the TBC—the maximum amount Geraldine can move into retirement phase.

The starting value of her account-based pension was $660,000, so this was the amount that counted towards her TBC.

In addition to this pension, Geraldine has a state government super pension currently paying $45,000 a year, but it started at $41,000 per annum. Accordingly, the amount of this ‘capped defined benefit income stream’ that counted towards her TBC was a ‘special value’ of $656,000 ($41,000 x 16).

Thus, the total amount counting towards Geraldine’s TBC is $1,316,000 ($660,000 + $656,000), well under the current $1.6 million limit.

So, if Geraldine takes $32,010 in pension payments, the amount counting towards her TBC remains unchanged at $1,316,000.

However, if she takes $16,010 as pension income and makes a $16,000 lump sum withdrawal, then the amount counting towards her TBC reduces to $1.3 million as the partial commutation of her pension comes off the amount counted, i.e. $1,316,000 – $16,000.

Subsequently, Geraldine sells her home and—being eligible—makes a ‘downsizer contribution’ of $300,000.

If Geraldine takes the $32,010 in pension payments, she can only transfer $284,000 ($1,316,000 + $284,000 = $1.6 million) into retirement phase where earnings, including capital gains, are tax-free, whilst $16,000 must remain in the taxable accumulation phase.

However, if she takes $16,010 as pension income and $16,000 as a lump sum withdrawal, then she can transfer the entire $300,000 into an account-based pension, i.e. $1,300,000 + $300,000 = $1.6 million.

If you go down the path of taking the amount above the minimum annual payment as a lump sum withdrawal, then you need to make a valid election requesting the trustee to treat the payment over the minimum as a partial commutation and this must be done before the payment is made.